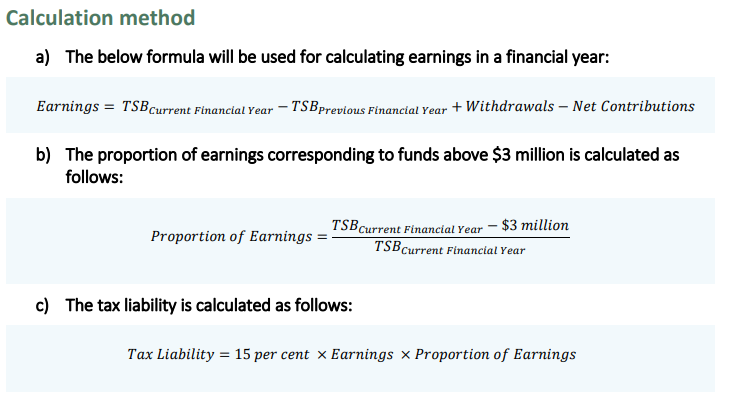

Example of a Balance exceeding $3 million

Warren is 52 with $4 million in superannuation on 30 June 2025. He makes no contributions or withdrawals. By 30 June 2026, his balance has grown to $4.5 million. Warren’s calculated earnings are: $4.5 million – $4 million = $500,000 His proportion of earnings corresponding to funds above $3 million is: ($4.5 million – $3 million) ÷ $4.5 million = 33% Therefore, his additional tax liability for 2025-26 is: 15% × $500,000 × 33% = $24,750

Warren is 52 with $4 million in superannuation on 30 June 2025. He makes no contributions or withdrawals. By 30 June 2026, his balance has grown to $4.5 million. Warren’s calculated earnings are: $4.5 million – $4 million = $500,000 His proportion of earnings corresponding to funds above $3 million is: ($4.5 million – $3 million) ÷ $4.5 million = 33% Therefore, his additional tax liability for 2025-26 is: 15% × $500,000 × 33% = $24,750

For more information about this targeted Superannuation concession, read the Fact sheet available from the ATO:

https://atotaxrates.info/wp-content/uploads/2023/03/better-targeted-superannuation-concessions-factsheet.pdf